Typical business banking challenges:

Although small businesses — defined as organizations with fewer than 500 people — represent 99.9% of all companies in the U.S., they often struggle to find banking solutions tailored to their needs.1

Large financial institutions, which have historically dominated the banking landscape, are well-versed in serving individual retail clients and large commercial banking customers. However, this paradigm has left small businesses without a solution that’s truly tailored to their needs.

Many business banking products offered by traditional banks have significant limitations, ranging from account minimums to low interest rates. Some may cap the number of fee-free monthly transactions or otherwise limit withdrawals. It’s not uncommon to see charges for essential business banking services, like ACH transfers.2

Within their own four walls, small businesses face additional challenges in managing their finances. Unlike their larger corporations, they often do not have dedicated finance teams, which may lead them to focus on managing the basics, such as cash inflow and outflow, rather than exploring opportunities to grow their business through strategic financial management. Without an in-house team, these small businesses may struggle to hold adequate reserves to meet short- and medium-term needs while remaining below the $250,000 FDIC-insured limit.

How Flourish Cash solves for these common business banking hurdles:

With Flourish Cash, business owners have access to a flexible cash account without the limitations of a traditional bank. A Flourish Cash business account offers all the same benefits of personal Flourish Cash accounts:

- No fees ∫∫

- No minimum balance requirements

- Unlimited, same-day transfers|

- Competitive APY§ that is up to 8x more than the national savings account average#

- Up to $7.5 million in FDIC insurance coverage through our Program BanksΩ

A Flourish Cash business account also offers clients versatility. For the business owner looking for an account to hold funds for their immediate needs – while still earning a competitive interest rate that can meaningfully contribute to profits – they are better served with unlimited, same-day transfers. For those looking for a more secure solution for medium- and long-term cash needs, they have access to an account that offers up to 30x more FDIC coverage through our Program Banks. For those working for a nonprofit looking for a way to maximize every dollar, moving funds from a traditional bank offers the opportunity to earn an interest rate up to 8x higher, which can translate to expanded initiatives.

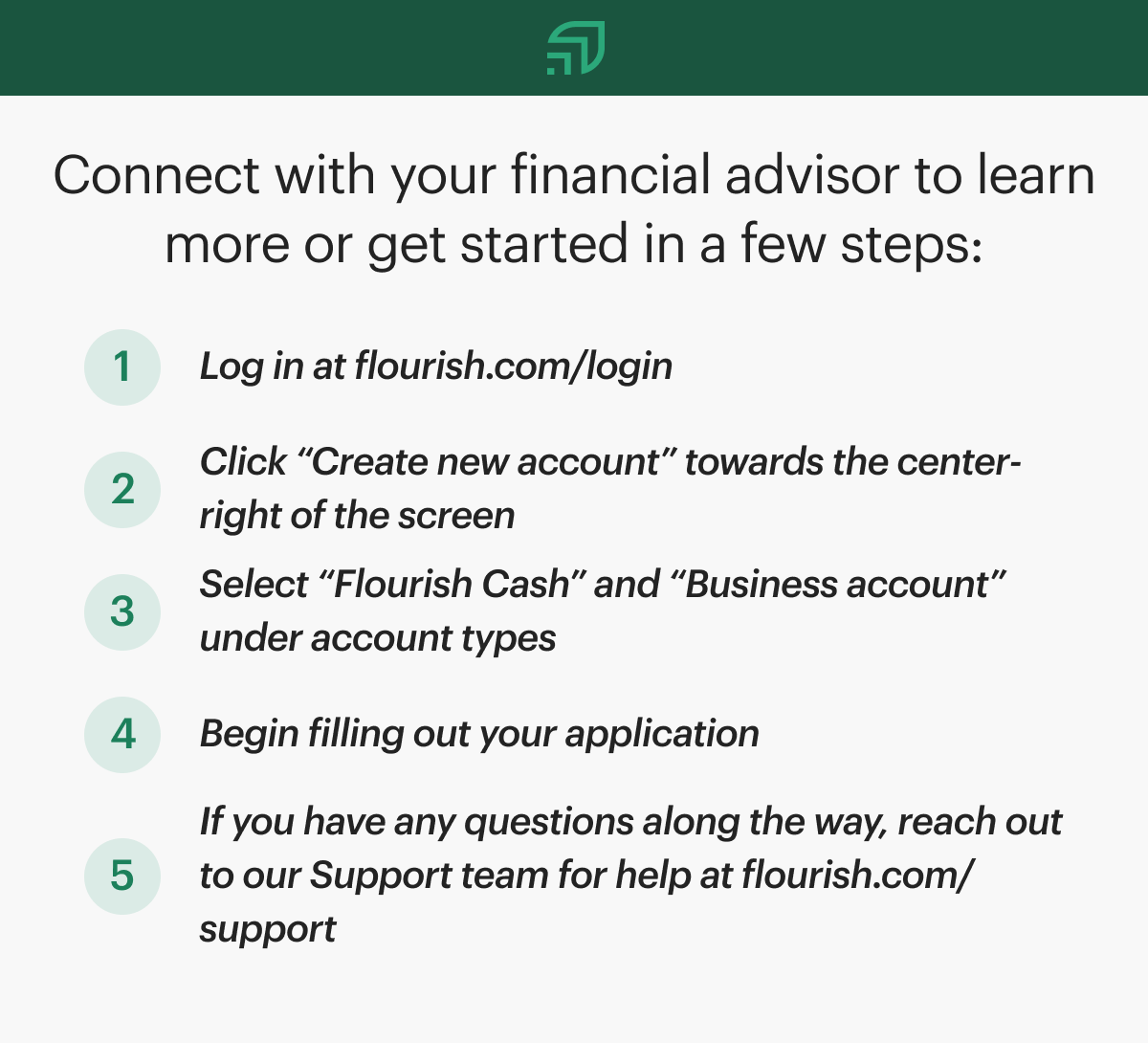

Log in

Log in