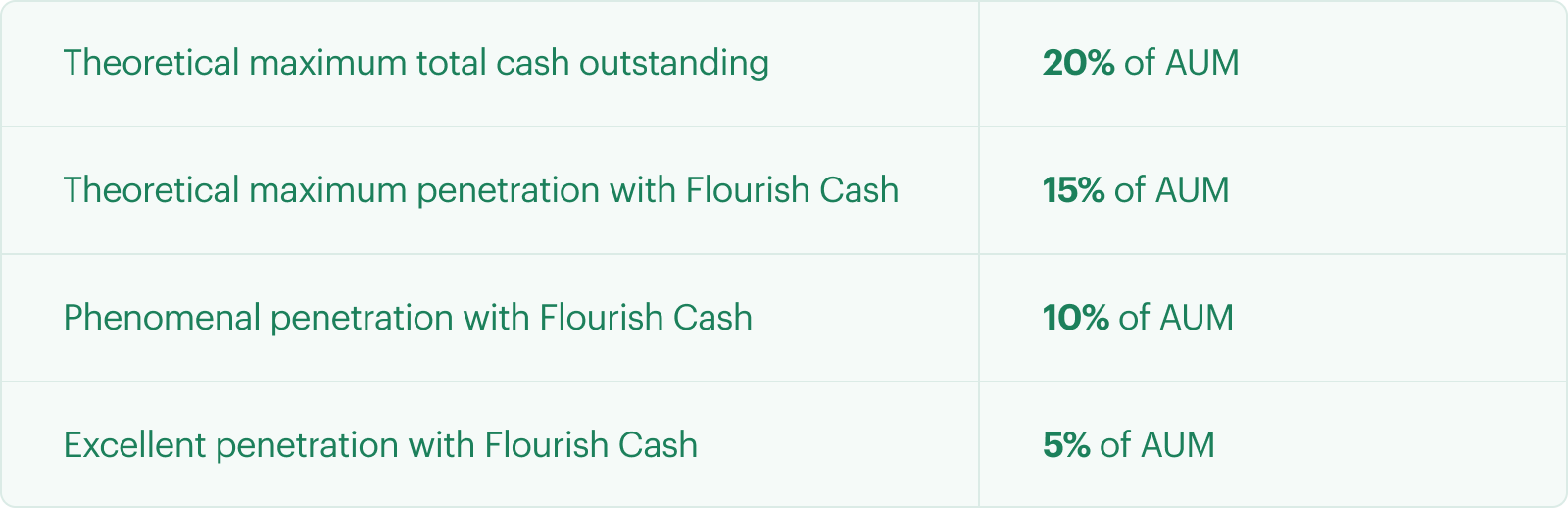

Numerous studies show that high net worth individuals (HNWIs) hold approximately 20% of their wealth in cash.1 From here, we make the assumption that roughly 20% of your firm’s AUM represents your clients’ total cash holdings. For a firm that manages $1B in assets for personal clients, that means your clients could have $200M+ in cash on the sidelines.

There are a variety of macroeconomic forces, personal traits, and life factors that can influence whether your clients hold more or less cash than the average investor. If you wish to adjust this baseline calculation, you can factor in specific details you know about your client base and adjust this 20% assumption upward or downward, as needed.

Some of a client’s decisions about cash are driven by behavioral factors. As an example, research from Vanguard showed that in 2022, as anxieties about the market rose, more clients tapped retirement funds and converted some of those assets into cash.2

A client’s stage of life may also influence the amount of cash they hold. Research shows that HNWIs of the silent generation hold an average of 23% in cash. In contrast, cash reserves for high net worth millennials represent 11% of their total assets.3

You know your broader client base and their needs in the current macroeconomic environment best, and so may wish to adjust our general 20% AUM assumption up or down to account for the realities of your book of business at any given time.

Log in

Log in

-3.png)

.png)

-1.png)

.png)

.png)

.png)

.png)

.png)